Battle-Hardened Energy Sector Faces Another War

March 2020

WHAT’S INSIDE:

The last time OPEC waged war on the oil market was November 2014. This created a challenging 2015/2016 but US production bounced back.

This price war is different thanks to the unprecedented drop in demand due to COVID-19.

It is expected that Canadian upstream spending will contract 20-30% from 2019

Investors have faced an uphill battle since 2013 and this sharp downturn reinforces the negative stigma of investing in energy

WHAT’S DIFFERENT ABOUT THIS OIL PRICE WAR?

November 27, 2014 - a date that will forever hang in our minds. Saudi Arabia rejected calls for a crude oil supply cut, signifying a price war against the emerging threat of US supply growth. Crude prices slid 10% that day, capping off a 35% fall over a 4 month timeframe and setting the stage for a further 33% decline in the following 2 months. The price collapse stalled out in January 2015 before taking another plunge late 2015/early 2016 which saw WTI prices dip below $30/bbl. This downturn was hard on the industry with capital spending, service costs and institutional investor support all undergoing a transformational change. And while the downturn did remove 0.6 mmbbl/d of US production, it was temporary as US production has since grown by 3.3 mmbbls/d.

Flash forward to today and while the headline price war is Saudi Arabia and Russia dominated, the North American industry sits in the crosshairs. We are in unchartered waters with demand suffering the largest shock on record and supply ramping from two of the largest exporters in the world. This is painting a negative storage picture that may require prices to hit shut in levels sooner than later. We take comfort in the fact that the industry has proven its resilience time and time again, but we are nervous that investors willing to support the industry have not.

WTI and WCS Price Movements since 2013 (US$/bbl)

WORLDWIDE CRUDE OIL DEMAND SHOCK

Energy forecasters are starting to roll out their estimates of demand destruction thanks to the current pandemic with a handful suggesting crude oil demand in the first half of 2020 could be down in excess of 8 million barrels per day. This would be the largest demand shock on record and, combined with increasing supply from Saudi Arabia and Russia, paints a very ugly picture. If we don’t see some capitulation from the price war (next scheduled meeting in June) and if COVID-19 continues to drag, world storage capacity will be tested putting the potential for large scale price driven shut in production a probable outcome.

COVID-19 Worldwide Crude Oil Demand Destruction Off the Charts

PLENTY OF CAPITAL AND THE PERMIAN DROVE MASSIVE US SUPPLY GROWTH

From 2012 to 2014, US Crude and Condensate supply rose over 2 mmbbls/d (35%) as the shale boom took hold. Despite the Saudi’s formally waging war against the US industry in late 2014, US production rose again in 2015. It took sub $30/bbl pricing in 2016 for US production to fall 5%, but this was quickly replaced with record production in 2018 and 2019. Thankfully today’s energy investors care more about return of capital and financial strength than production growth, meaning upstream producers will be more willing to have production decline in order to preserve value. Depending on the duration of the demand destruction from COVID-19, a natural decline in US production is likely not enough to avoid disaster.

US Crude Oil Growth

HOW DOES THIS IMPACT THE CANADIAN ACTIVITY OUTLOOK?

Late 2019 and early 2020, optimism was in the air with indications pointing to a more robust year for Canadian upstream spending compared to 2019. COVID-19 was the first headwind pushing WTI prices towards $45/bbl when OPEC+ failed to reach an agreement sending prices south of $30/bbl and WCS to the lowest on record. Spending budgets continue to be adjusted in this new reality with expectations calling for 20-30% less spending than 2019, which was the lowest capital spending program in the last 10 years. Thankfully, the last three years have seen producers spend less than cash flow, cleaning up their balance sheets in the process making them more resilient.

Canadian Upstream Spending

Canadian Upstream Spending vs. Cash Flow

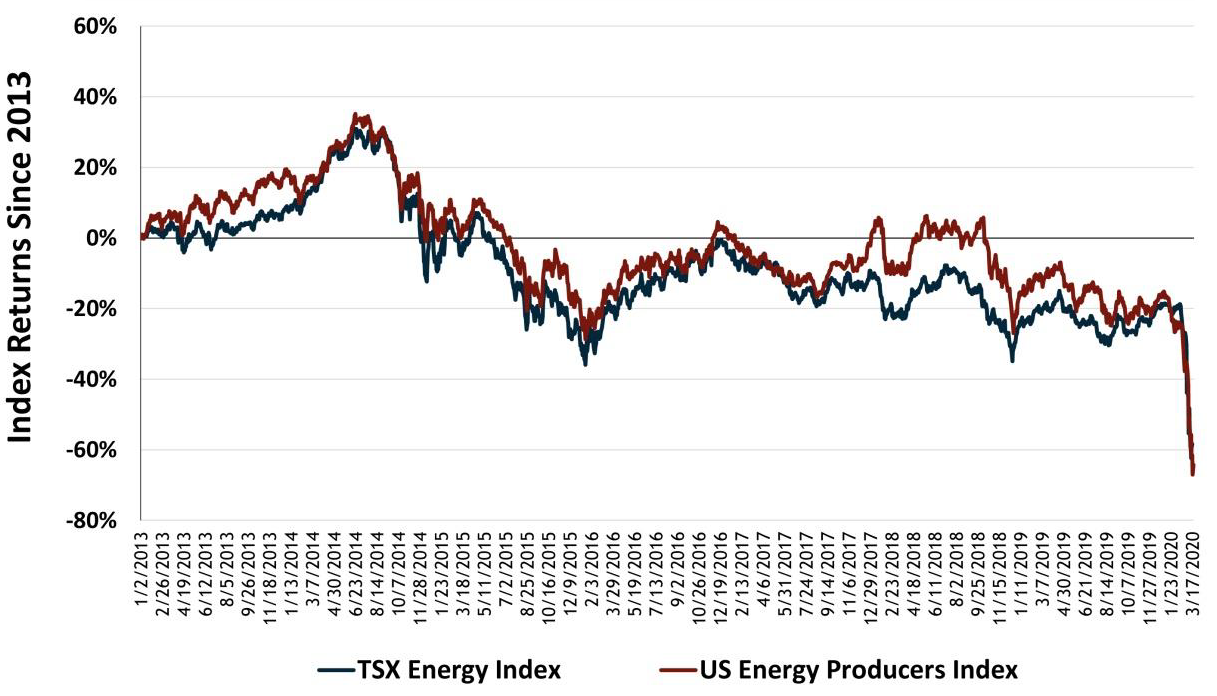

North American Energy Sector Returns

WILL THERE BE ANYONE LEFT TO CARE?

Yes, we will get through this price war, and yes there will be casualties despite how battle-hardened Canadian producers have become. We are concerned one of the larger casualties may be a lack of investors willing to put money to work in the sector. Investing in the North American energy space has seen many of the best investment minds fall to the wayside as the risk return profile has not been aligned for quite some time. Like after the 2016 downturn, we hope what emerges is a stronger energy sector, with an increased focus on value creation and ultimately primed for the next battle.

Sources: Bloomberg, Diamond Willow Advisory, BP, ARC Financial, Company reports